TL;DR: The 2024 LLM trading edge has already been arbitraged — Lopez-Lira’s famous GPT long-short strategy has decayed from a 355% backtest (Sharpe 3.05) to roughly 51% directional accuracy on headline reactions by late 2025, as 95% of hedge funds now run GenAI. In 2026, the only durable moat is the speed of the adaptation loop: regime-aware agents that re-train, re-validate and re-deploy in hours, not quarters. Funds that ship compliance-by-design, anti-crowding strategy discovery and multi-agent research fleets this year will compound an information advantage the rest of the street can no longer buy with headcount.

Why has the 2024 LLM trading edge already decayed?

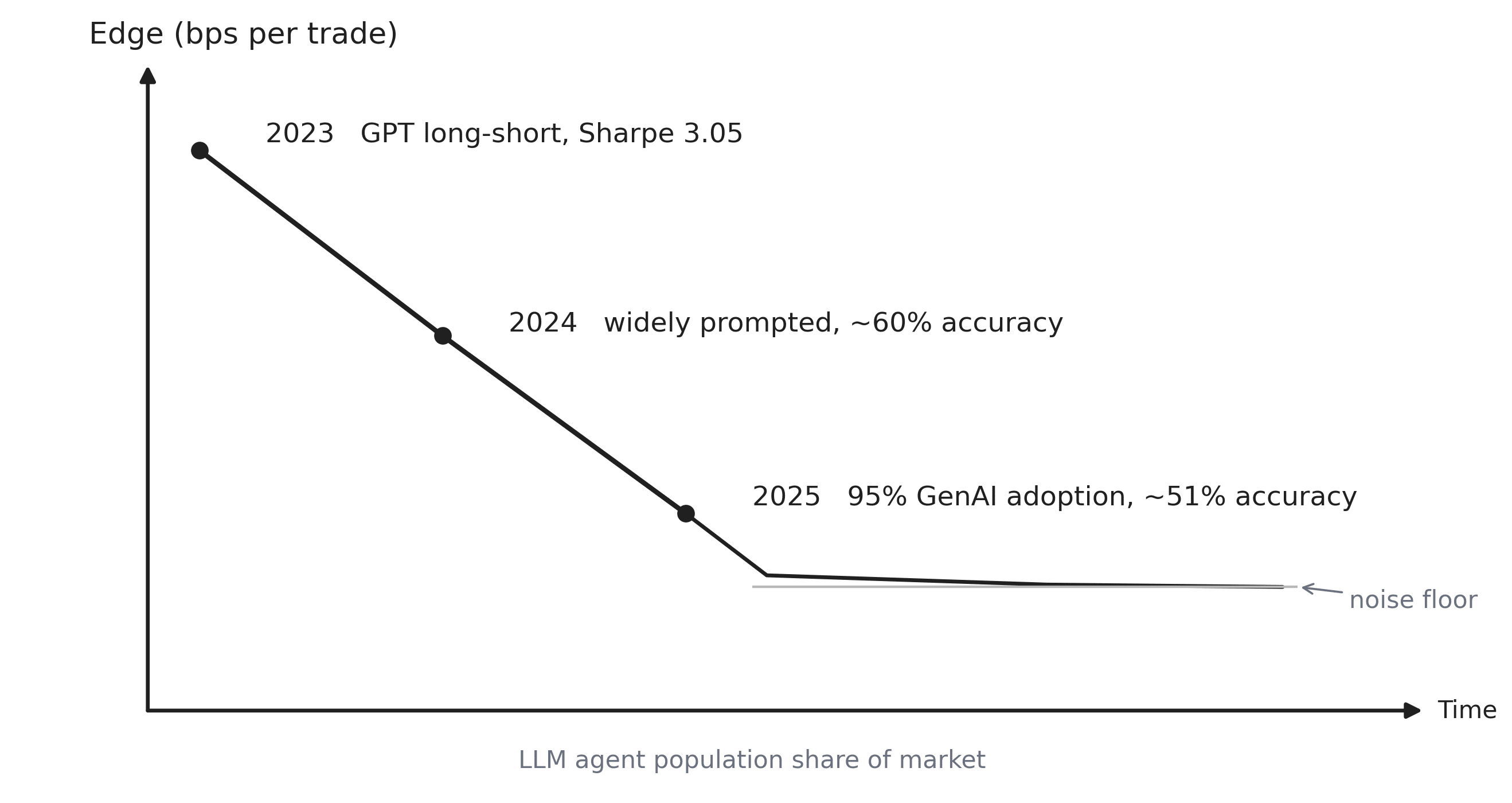

The single most-cited GenAI trading result of the last cycle — Lopez-Lira’s GPT-powered long-short strategy — printed a 355% cumulative return at a Sharpe of 3.05 in backtest and has since collapsed to roughly 51% directional accuracy on headline reactions by late 2025. The authors themselves wrote that “strategy returns decline as LLM adoption rises, consistent with improved price efficiency” — in plain English, the paper killed its own alpha by being read.

What does “51% accuracy on headline reactions” actually mean?

It is the simplest possible score for a news-driven trader: given a fresh headline (e.g. “Company X beats EPS by 12%”), the model predicts whether the stock will close up or down over the next trading interval. A coin flip is 50%. A score of 51% means the strategy is right about one out of every hundred headlines more often than random — after trading costs, slippage and borrow, that is statistically indistinguishable from noise. The same model was scoring materially above 60% in 2023, which is where the 355% backtest came from; the 9–10 percentage-point collapse is the entire alpha, erased by diffusion.

That is not a fluke; it is the base rate for 2026. AIMA’s hedge-fund surveys show GenAI usage jumped from 86% (Dec 2023) to 95% (Sep 2025), and the share of managers who expect GenAI to drive investment decisions within a year rose from 20% to 58%. When 95% of the population runs the same frontier models on the same public filings, the half-life of any public signal shrinks to the time it takes to diffuse across that population.

Diagram: The alpha diffusion curve

Source: synthesised from Lopez-Lira returns decay and AIMA adoption surveys.

What exactly changed in 2026 for regulated AI trading?

Regulators have just promoted “agentic” from a buzzword to a first-class regulated category, and the calendar is tight:

Bolting compliance on after launch is no longer survivable — LPs and internal counsel will gate funds that cannot show citations, supervisor agents and kill-switches on day one. AI-related 10-K mentions of “AI agent” are already up 6,550% year over year, confirming the arms race has hit disclosure.

Why do naive LLM agents collapse in adversarial markets?

Because they default to fixed playbooks. The February 2026 TraderBench study (arXiv 2603.00285) put 13 frontier LLM agents through four progressive market-manipulation regimes — spoofing, layering, narrative attacks on news sentiment and coordinated sentiment flips. 8 of the 13 leading agents held a flat ~33-point score across all four regimes, meaning they never adapted their strategy when the market started gaming them.

Translation for a PM: if your agent cannot detect that another agent is gaming it, your edge is a liability. Treat trading agents like a security perimeter — red-team them weekly, not annually.

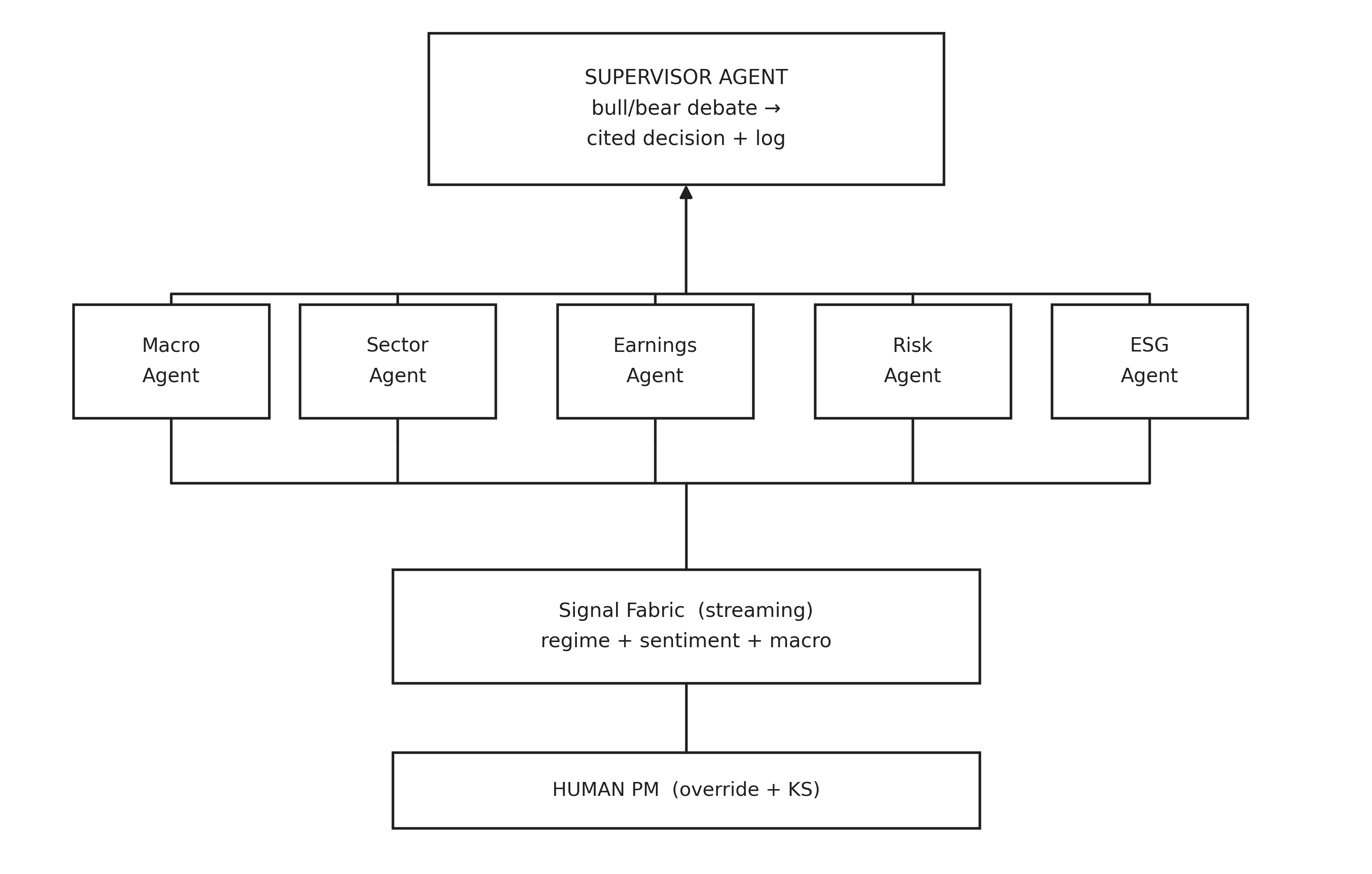

What does a multi-agent trading organisation actually look like?

The winning architecture mirrors a real trading desk: specialised agents debating under a supervisor, with humans on the override switch. To make this concrete, here is what each agent does, with a realistic example of its output on a single ticker (say, TSMC ahead of earnings):

Diagram: Multi-agent debate under a supervisor

Columbia/BlackRock research shows three-layer multi-agent frameworks with explicit bull/bear debate agents consistently outperforming the S&P 500 by externalising cognitive tension — one-model funds will soon look like one-PM funds.

What is the actual durable edge in agentic trading?

Six edges are worth anchoring a 2026 AI trading strategy on — pick two or three and execute ruthlessly:

- Speed of adaptation > speed of inference. The HFT race ended at nanoseconds; the agentic race is measured in hours between regime detection and strategy redeployment. Funds that re-deploy in hours eat funds that re-deploy in quarters.

- Anti-crowding by construction. The 2026 QuantaAlpha paper (arXiv 2602.07085) names “factor crowding and accelerate decay” as the central risk of LLM alpha mining — enforce diversity at generation time via genetic search and trajectory-level mutation, not ex-post correlation filters.

- Adversarial robustness as a product spec. If TraderBench breaks 8 of 13 frontier agents, assume yours is in the 8 until you prove otherwise.

- Compliance-by-design. Citations, supervisor agents, kill-switches and named human accountability ship with v1 — not v3.

- Multi-agent org chart. Debate beats monologue.

- Coverage multipliers, not headcount. An analyst who covered 20 names now covers 200 with an agent fleet; 44% of finance teams already use agentic AI in Q1 2026 — a 600% year-over-year jump.

What does the evidence actually show?

How does RocketEdge’s stack map to the 2026 shift?

| 2026 Imperative | RocketEdge Product | What It Does |

|---|---|---|

| Speed of adaptation | MultiEdge AI Signal Fabric | Streams regime detection (HMM/LSTM), sentiment and macro nowcasts as machine-readable features for autonomous agents |

| Anti-crowding strategy discovery | AI Trade Idea Generator | RL + genetic algorithms explore millions of combinations; triple-layered anti-overfit pipeline rejects 94%, CPCV and deflated Sharpe survive |

| Multi-agent org chart | Agentic Research Platform | Macro, Sector, Risk, ESG and Earnings specialists debate under a Supervisor Agent on Azure AI Foundry Agent Service — every claim cited to source |

| Compliance-by-design | Cross-stack | Plain-language rationale per trade, drawdown-enforced supervisor, auditable logs to Power BI/Excel, deploys inside the client’s own Azure tenant |

| Coverage multiplier | MultiEdge memos | Pre-meeting research memos in hours, covering 5x more names with the same team |

Availability: The full RocketEdge stack (Trading GPT engine + MultiEdge Signal Fabric, Agentic Research Platform and AI Trade Idea Generator) is entering design-partner previews in Q3 2026, with general availability on Azure Marketplace in Q4 2026.

What this means for your trading desk this quarter

- Measure your redeployment latency. If it is longer than a trading week, you are structurally short alpha.

- Audit every live strategy for public-paper risk. If its logic appeared in an arXiv preprint in 2023–2024, assume it has been arbitraged.

- Red-team one agent against spoofing and narrative attacks this month using the TraderBench protocol.

- Write the JD for your “named human accountable per agent” before MAS, the Fed or your LP asks — the deadline is August 2026.

- Pilot a multi-agent debate layer on one sleeve of the book — bull/bear specialists under a supervisor — and benchmark against your single-model baseline.

FAQ

What is agentic trading in 2026?

Agentic trading is a system where specialised AI agents (Macro, Sector, Earnings, Risk, ESG, Execution) operate under a Supervisor Agent to autonomously generate, validate and deploy trading decisions with cited reasoning and auditable logs. It is distinct from static algos because the loop — not the model — is the edge.

What does 51% accuracy actually mean for an LLM trading strategy?

It means the model predicts the correct post-headline direction (up or down) roughly 51 out of 100 times — only one percentage point above a coin flip, and statistically indistinguishable from noise once trading costs are included. That is the state to which a 355% backtest decayed once 95% of the industry was running the same frontier models.

Why has LLM-driven alpha decayed so fast?

Because 95% of hedge funds now prompt the same frontier models on the same public data, making any signal derived from that stack homogeneous and quickly arbitraged. QuantaAlpha (arXiv 2602.07085, 2026) names factor crowding as the dominant 2026 decay mechanism.

What regulations apply to agentic AI trading in 2026?

MAS’s AI Risk Management Toolkit (20 Mar 2026), the Fed/OCC/FDIC replacement of SR 11-7 via OCC Bulletin 2026-13 (17 Apr 2026), and EU AI Act Phase Two (2 Aug 2026) all cover agentic AI explicitly — requiring named human accountability, traceable decision chains and reproducible audit trails.

Do multi-agent trading systems actually outperform single-model ones?

Columbia/BlackRock research on three-layer multi-agent frameworks with bull/bear debate agents shows consistent outperformance of the S&P 500, while TraderBench shows 8 of 13 single-agent LLMs collapse under adversarial market manipulation.

When is the RocketEdge stack available?

Design-partner previews open in Q3 2026, with general availability on Azure Marketplace in Q4 2026 across all three products — MultiEdge AI Signal Fabric, the Agentic Research Platform and the AI Trade Idea Generator.

References

- Lopez-Lira — “The 355% Trade: How LLMs Quietly Hijacked” — Data’s Substack.

- AIMA GenAI Hedge Fund Survey (Dec 2023 → Sep 2025) — cited via Data’s Substack and Sify.

- Sify — “The dawn of hedge agents: how agentic AI is transforming hedge fund operations.”

- MAS — AI Risk Management Toolkit for the Financial Sector (20 Mar 2026).

- OCC Bulletin 2026-13 — Replacement of SR 11-7 (17 Apr 2026).

- Kiteworks — AI Regulation 2026 Business Compliance Guide (EU AI Act Phase Two).

- TraderBench (arXiv 2603.00285, Feb 2026) — adversarial robustness of LLM trading agents.

- QuantaAlpha (arXiv 2602.07085, 2026) — factor crowding and decay in LLM alpha mining.

- QuantSignals — “Static alpha is dead alpha.”

- Ragnar S. Ragnars — Columbia/BlackRock three-layer multi-agent framework commentary.

- Wundertrading — “Agentic Trading.”

- Nasdaq — “2026 SEC Disclosure Trends: AI Risk Factors” (6,550% YoY rise in “AI agent” 10-K mentions).

- AI Magicx — “Agentic AI finance & banking deployments 2026” (44% of finance teams, 600% YoY).

- Numerai — “NumerCon 2026: Genesis to Singularity.”

- ZenML — “Agentic AI architecture for investment management platform” (BlackRock Aladdin Copilot, $11T AUM).