TL;DR. Dwarkesh Patel’s “The AI Firm” essay — turned into a stunning, fully AI-generated video sponsored by Google — argues that once AGI arrives, companies stop being made of people and become armies of copyable, mergeable, evolvable digital minds directed by a super-CEO (“Mega-Sundar”). The digital-labour insight is real and underrated. But the load-bearing assumption underneath it — that you can copy judgment, tacit knowledge, and coordination the way you copy a file — is exactly the assumption that Hayek, Mises, and Coase already refuted a century ago. The AI firm as described is Gosplan with GPUs: a central planner that abolishes the very price signals and dispersed knowledge it needs to function. More compute doesn’t dissolve the knowledge problem. It just lets you fail faster, at higher fidelity, with total surveillance. The durable edge in AI trading isn’t headcount-in-GPUs — it’s human-in-the-loop judgment applied to proprietary, real-world data the market itself generates.

What is “The AI Firm,” and what does it actually get right?

In January 2025, Dwarkesh Patel — with Ege Erdil and Tamay Besiroglu of Epoch AI — published “What fully automated firms will look like”, flagged with the honest epistemic status “Shooting-the-shit; 25% sure.” Months later it became a companion video — every frame generated by Google’s Veo model, sponsored by Google.

The argument has five moves, and each is genuinely sharp:

- Copy. Firms are bottlenecked on hiring and training. If your best engineer is software, clone them a million times “with all their skills, judgment, and tacit knowledge intact.” Turn capital into compute and compute into labour.

- Merge. A human CEO’s model of their company is “necessarily incomplete.” Mega-Sundar absorbs everything millions of distilled copies see — “every customer conversation, every engineering decision, every market response” — so there is “approximately no miscommunication, ever again.”

- Scale. The cost of a role collapses to the compute it consumes. The CEO function justifies $100 billion a year of inference, running “Monte Carlo simulations of different five-year trajectories.”

- Evolve. Human firms “can’t replicate themselves” because they’re “made of people, not interchangeable, easily copied widgets.” AI firms can clone winners — a leap “like the gulf in complexity between prokaryotes and eukaryotes.”

- Takeover. So does the first firm to fully automate become the last company standing? Patel checks himself: internal planning “needs to be constrained by some slower but unbiased outer feedback loop” — the market.

Give it its due. The copyability asymmetry between digital and biological workers is real, underexplored, and correctly identified as the thing most people miss when they picture AGI as “a smart assistant that works 24/7.” The essay cites Coase and Gwern rather than ignoring the economics. It flags its own confidence at 25%. This is a serious intellectual contribution, and it deserves a serious rebuttal — not a dunk.

But here is the tell. The essay names its own gravediggers and then waves them away with a single sentence: “the balance may shift as AI systems improve.” That sentence is carrying the entire argument. And it is the precise error that economics spent the twentieth century refuting.

Why is “the balance may shift as AI improves” the fatal flaw?

Because it treats a problem of kind as a problem of degree.

Let me apply the first of two named mental models I’ll use throughout: first-principles reasoning — stripping the claim to its economic fundamentals rather than reasoning by analogy to today’s org charts.

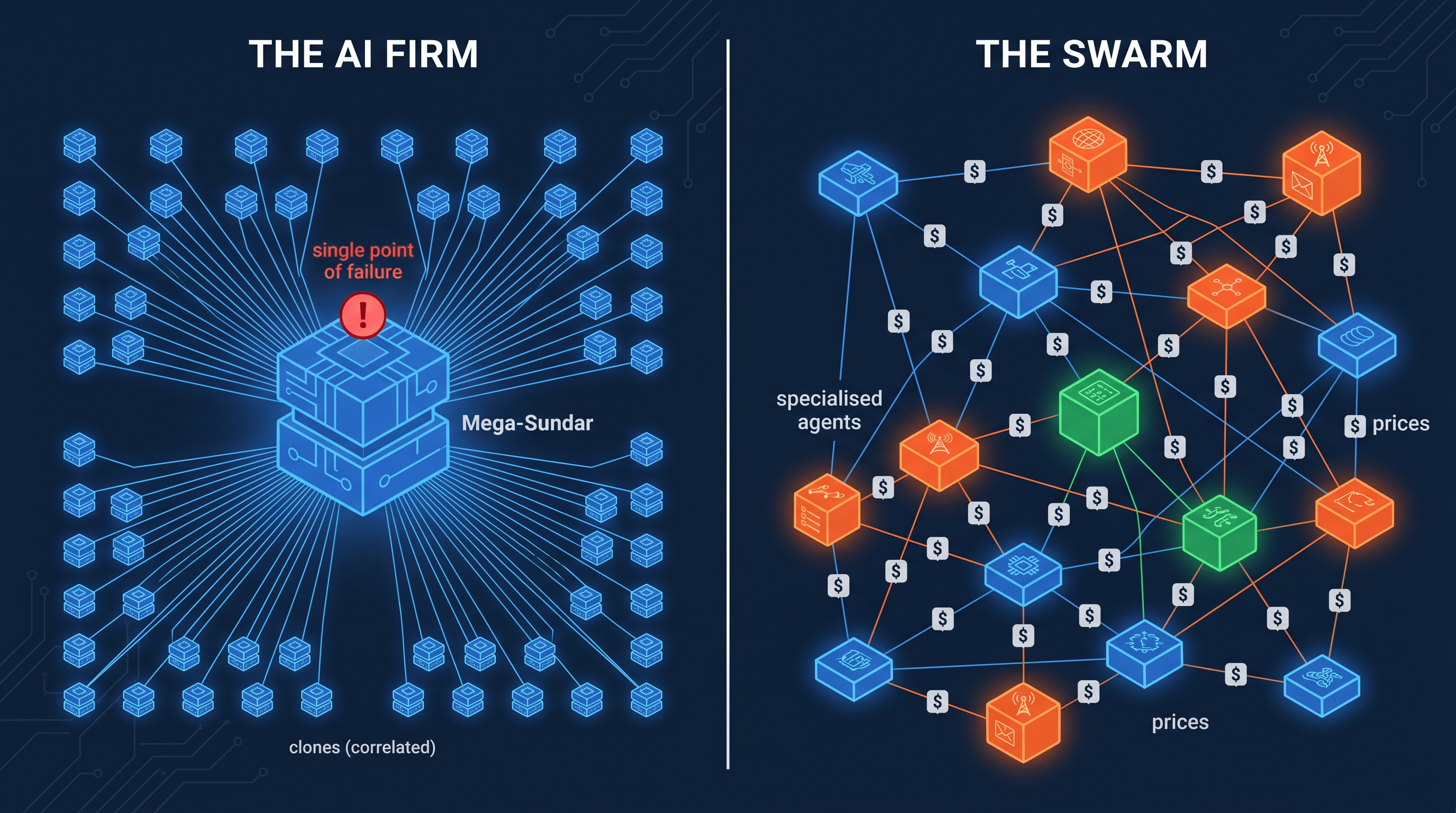

Reduced to first principles, Mega-Sundar is a central planner: one mind that ingests all information, computes the optimum, and directs all production from the centre. Patel even reaches for the vocabulary himself — a “politburo-style” board, millions of “distilled Sundar apparatchiks.” The irony is meant to be knowing. It cuts the wrong way.

This is the socialist calculation debate, reborn with a GPU cluster. And the objection that killed central planning was never “the planners are too slow” — a concession that faster computers would fix. Let me diagnose the stated cause versus the actual cause:

- Stated cause of central planning’s failure (the essay’s implicit model): planners lacked processing power and real-time data. Assessment: fails. The USSR had rooms full of economists and, later, computers. Chile’s Project Cybersyn (1971–73) wired the economy to a central operations room fed by real-time telex — a literal 1970s Mega-Sundar. Its own historians concede the technology “was unlikely to have been up to the task,” but the deeper failure was structural, not computational.

- Actual cause (Hayek, 1945): the knowledge required to coordinate production “cannot enter into statistics and therefore cannot be conveyed to any central authority in statistical form.” It is dispersed, tacit, contextual, and — critically — generated only by the decentralised process of people acting and exchanging. Assessment: holds.

Keyword, with a concrete example. The knowledge problem is not “we don’t have the data.” It’s that the decisive knowledge doesn’t exist in extractable form until the market creates it. When a Jakarta warehouse manager senses a supplier is about to miss a shipment because the man’s voice was off on the phone, that judgment never becomes a row in a database. It exists only in the doing. Mega-Sundar can have every byte the firm ever recorded and still not have that knowledge — because the knowledge isn’t in the bytes.

As the economist Heng-Fu Zou puts it in his 2025 restatement of Hayek for the AI age: “AI can process data, but data are not identical to knowledge; AI can predict, but prediction is not discovery; AI can simulate prices, but simulated prices are not market prices generated by property, exchange, competition, profit, and loss.”

Premise → reasoning → conclusion. Premise: rational coordination requires dispersed, tacit, locally-generated knowledge. Reasoning: that knowledge cannot be centralised into one mind at any compute budget, because it doesn’t exist in centralisable form. Conclusion: Mega-Sundar’s core function — total context in one head — is not expensive. It is impossible in principle. No FLOP count closes the gap.

Mises’s point is even sharper, and the essay misses it entirely: without private ownership and exchange of capital goods, there are no real prices for those goods, so rational calculation is impossible. A firm that internalises its whole value chain into one Mega-Steve destroys the very price signals it needs to allocate capital. The bigger the conglomerate, the blinder it gets. This is not a bug the essay overlooked. It is the essay’s endpoint.

What historical precedent tells us how this ends?

The precedent isn’t speculative. We ran the experiment.

Precedent 1 — Oskar Lange’s market socialism (1930s). Confronted by Mises, the economist Oskar Lange conceded the planner couldn’t know the prices — but argued a planning board could simulate the market by trial and error, iterating toward the invisible hand. “$100 billion of inference running Monte Carlo on five-year plans” is the Lange move with better hardware. The economists Boettke and Candela named the modern genre — technosocialism — and explained why it keeps failing. Jack Ma made the identical bet in 2017: “big data will let us finally achieve a planned economy.” Same fallacy, new decade.

Precedent 2 — the 1960s–70s conglomerate wave. ITT under Harold Geneen and Gulf+Western under Charles Bluhdorn tried to run “a grab bag of companies” under single central management. They were largely dismantled in the 1980s–90s. The financial residue is measurable: diversified conglomerates trade at a 13–15% average value discount (Berger & Ofek, Journal of Financial Economics, 1995), driven by “overinvestment and cross-subsidisation” — exactly the internal-misallocation pathology you get when central management can’t calculate.

Analogy (and its limit). Mega-Sundar is Cybersyn with a trillion-dollar data centre instead of a telex network. Where the analogy breaks down: Cybersyn was trying to run a whole national economy; an AI firm is one company inside a market, so it does retain an external price signal — for now. But that concession is the essay’s undoing, not its defence, as we’ll see when we get to Coase.

Bigger context — why now, and where it goes. Two forces converge. One is secular: the cost-of-compute curve has fallen far enough that “turn capital into labour” feels within reach, so the old planning dream returns wearing an AI costume. One is cyclical: we are near the top of an AI-infrastructure capex supercycle, and grand centralisation narratives always peak with the capex. The IEA projects data-centre electricity demand more than doubling from ~415 TWh in 2024 to ~945 TWh by 2030 — roughly Japan’s entire consumption — with ~20% of planned projects at risk of grid-driven delays. “Turn capital into compute into labour” treats compute as frictionless at the exact moment power became the binding constraint.

Can you actually copy judgment? (No — and here’s the proof)

This is the assumption in the title, and it is where the whole edifice rests: copying an engineer “with all their skills, judgment, and tacit knowledge intact.”

Here is my second named mental model: the map–territory distinction. The weights of a model are a map. Judgment operates on the territory — the specific, novel, reflexive situation in front of you. The essay assumes a perfect map is the same thing as competence on the territory. It isn’t.

Three independent failures stack up:

1. Polanyi’s Paradox — the knowledge you most want to copy is the knowledge that can’t be codified. Michael Polanyi’s foundational insight (The Tacit Dimension, 1966): “We know more than we can tell.” Tacit knowledge — the negotiator’s read of a room, the risk manager’s nose for a position that’s “too clean” — is by definition what resists articulation. This is Polanyi’s Paradox (Autor, 2014), and it’s why automation has repeatedly struggled with tasks humans find trivial. The category error is fatal in the essay’s own terms: if an AGI has genuinely acquired tacit judgment, it acquired it through experience, not by having it “copied in” — and you can copy weights perfectly, but you cannot first get the un-codifiable knowledge into the weights. The hard part is assumed solved. That is the entire question, begged.

2. A million clones is one mind wearing a million hats. The essay’s “population size → more ideas” claim quietly swaps headcount for variation. But discovery comes from variation, not population. A million copies of one base model share the same priors, the same blind spots, the same failure modes. Epistemically, 10⁶ correlated clones are closer to one agent than to a million humans. And “merge-and-reabsorb” makes it worse — it’s variance reduction, the opposite of the diversity discovery requires.

3. Model collapse — the org eats its own exhaust. The “merge” mechanism has a specific, empirically demonstrated failure mode. Shumailov et al., Nature 631:755–759 (2024) proved that training generations of models on their own output “causes irreversible defects… in which tails of the original content distribution disappear” — variance shrinks, novelty dies, “the latest model becomes useless.” Crucially, this holds even with infinite samples and no estimation error. A firm whose central intelligence learns primarily from its own distilled sub-agents is running exactly that recursive loop. The “collective brain” is, in the limit, an echo chamber with a feedback loop.

Keyword, with a concrete example. Model collapse: fit a model to real data, generate synthetic data from it, retrain on the synthetic, repeat. In the Nature experiment, text about medieval architecture degraded into a list of jackrabbits by the ninth generation. Now imagine that dynamic inside a firm that has fired the humans who produced the only genuine data — which brings us to the parasite problem.

The AI firm is a parasite on the human host. Today’s models are distilled from human-generated data and human feedback (RLHF). The intelligence the essay wants to copy was paid for by the humans it proposes to replace. Fire the last human who generates real-world data, and you sever the training signal that made the copy valuable in the first place. Superintelligence that only listens to copies of itself starts, provably, to forget.

The self-refutation: perfect copying kills the evolvability it promises

This is the essay’s deepest internal contradiction, and it’s worth stating plainly because it’s the most shareable point in this entire piece.

Patel’s climactic argument is that AI firms win because they are evolvable — they can replicate winners like software or DNA. But evolution is not replication. Evolution is variation + selection + differential survival. Perfect, lossless copying of a single winner eliminates the variation selection acts on.

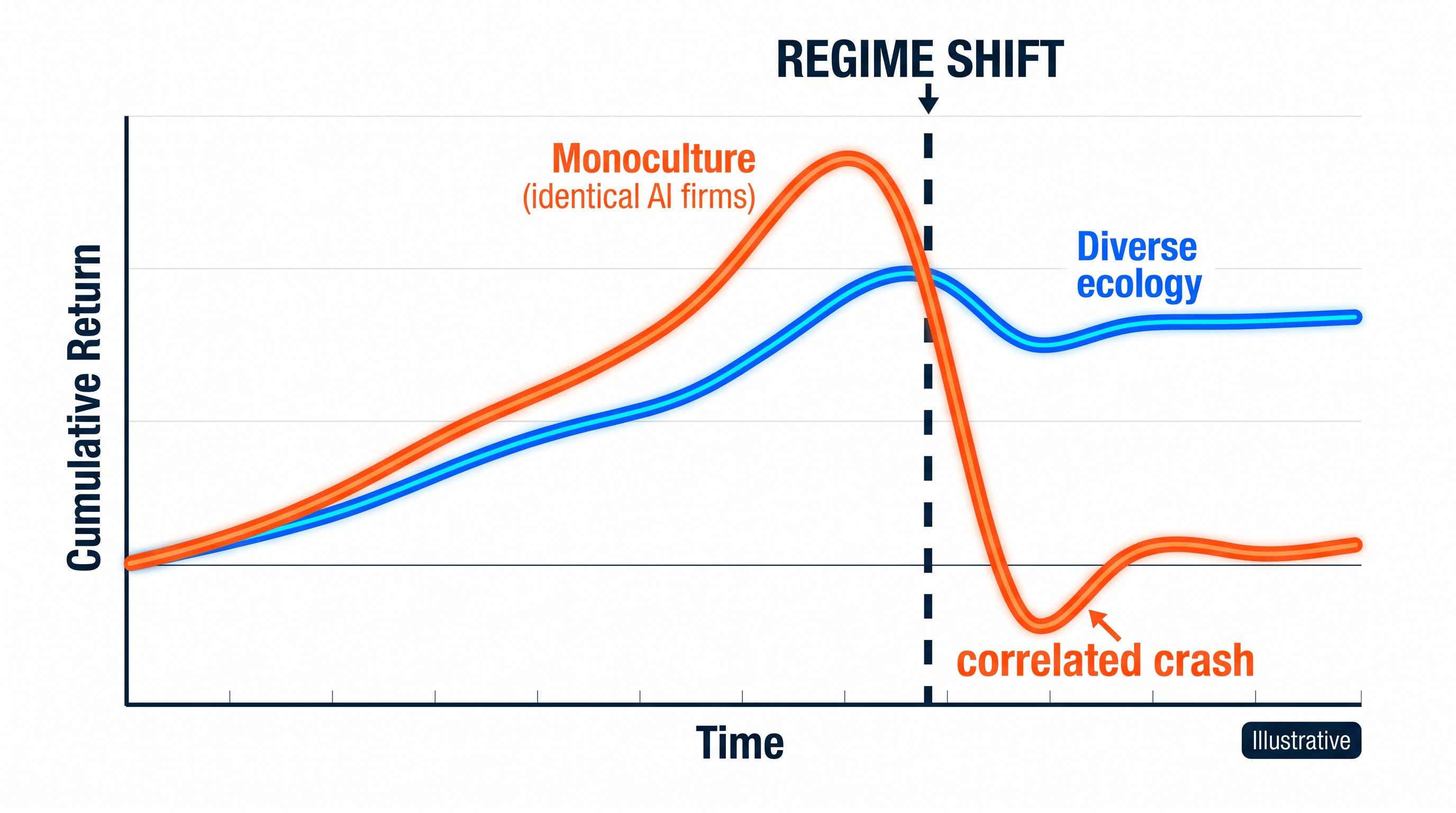

Biology is blunt about the destination. Strict clonal reproduction is an evolutionary dead-end in complex organisms; clonal lineages are short-lived and accumulate defects (Muller’s ratchet). And the essay’s own showcase metaphor argues against it: the prokaryote-to-eukaryote leap it invokes was enabled by endosymbiosis — the merger of different organisms — and sexual recombination. Evolvability came from symbiosis of the unlike, not cloning a champion bacterium a billion times. (The essay’s own footnote, correcting the metaphor, concedes this.) A firm that clones Mega-Sundar across every vertical and merges all learning into one mind has built the ultimate monoculture: maximally efficient, minimally evolvable, one shared blind spot from extinction.

And quants know exactly what a monoculture of correlated models does, because we’ve watched it blow up three times.

| Event | Mechanism | What broke |

|---|---|---|

| 1987 Black Monday | Portfolio insurance | Many funds ran the same model and mechanically sold into a falling market together |

| 2007 Quant Quake | Correlated stat-arb positions | “A coordinated deleveraging of similarly constructed portfolios” (Khandani & Lo, NBER 2008) |

| 2008 GFC | Shared VaR assumptions | Banks “failed because they were right in the same way” about mortgage correlation |

A commenter on Patel’s own post makes the point cleanly, invoking Taleb: an economy of identical AI firms is fragile — “a mistake in one copy will be spread everywhere, ~immediately.” Diversity isn’t inefficiency. It’s the system’s insurance policy. Cybernetics gave us the formal version decades ago — Ashby’s Law of Requisite Variety: “only variety can absorb variety.” A controller that regulates a high-variety world by reducing itself to one coherent vision is moving in precisely the wrong direction.

Why Coase dissolves the gigafirm instead of building it

Here’s the reversal the essay walks right up to and then declines.

Patel invokes Ronald Coase’s “The Nature of the Firm” (1937) to suggest that if AI slashes intra-firm coordination costs, firms grow enormous — maybe to “one gigafirm that consumes the entire economy.” But Coase is a theory of boundaries, not of growth. A firm expands only until the cost of organising one more transaction internally equals the cost of doing it through the market. The reason no firm swallows the economy is diminishing returns to management — internal coordination costs rise with scale.

Now trace the second-order effect (a third mental model, invoked by name: second-order effects — consequences of consequences). If AI collapses coordination costs inside the firm, it collapses them in the market too — arguably more, because market participants hold the local knowledge that Mega-Sundar structurally can’t. Cheap coordination doesn’t favour a Death Star. It favours a swarm of small, specialised agents transacting through prices. The essay picks the monopoly horn arbitrarily, when its own cited theorem points the other way.

This is the edge perspective almost no one has stated: the AI-firm thesis and its opposite are built from the same premise. Cheap machine coordination is real. But the equilibrium it produces is more decentralisation, not less — a market of millions of specialised agents, grounded in prices, out-evolving any monoculture. The gigafirm isn’t the destination. It’s the thing the market selects against.

How RocketEdge approaches this

We build AI trading infrastructure for a living, so this isn’t abstract for us. Our architecture is a deliberate bet against Mega-Sundar and for the swarm.

The MultiEdge AI Signal Fabric delivers signals as machine-readable features — regime detection, cross-asset momentum, alternative-data signals — for your models to consume, not as a single oracle’s verdict. We assume you keep your proprietary edge and your human judgment; we feed them better inputs. The Agentic Research Platform deliberately uses five specialised agents — Macro, Sector, Risk, ESG, Earnings — under a Supervisor, not one monolith, precisely because heterogeneity beats a monoculture and citation-verified outputs keep a human in the loop. And our anti-overfitting stack — walk-forward analysis, combinatorial purged cross-validation, deflated Sharpe ratio — exists because we treat backtests as a map, never the territory. That’s the whole philosophy: real proprietary data, diverse specialised agents, human judgment at the decision point.

Alternative Perspectives

Contrarian view 1 — Dwarkesh might be right on a long enough timeline, and the honest quant should say so. If three benchmarks move, the central-planning critique weakens materially: (a) if METR’s task-completion horizon reaches reliable multi-week autonomy at the deployment-relevant 80% threshold — today it’s ~16 hours at 50% but only ~3 hours at 80%; (b) if a demonstrated method lets models learn indefinitely from self-generated data without collapse (accumulate-real-data mitigations are promising but partial — Gerstgrasser et al., 2024); and (c) if a large firm demonstrably runs core strategy through one centralised model and beats a decentralised, market-tested portfolio of rivals over a full cycle. Watch those three. Intellectual honesty demands we name our own kill criteria.

Contrarian view 2 — this is 1984, not GPT-5, and that’s the real story. Read the “merge everything Mega-Sundar sees” architecture as a political document, not an efficiency memo. A single mind absorbing “every customer conversation, every engineering decision,” with “surgical modification of the weights to encode specific insights,” is a panopticon with write-access to its subjects’ minds. Concentration of information is concentration of power. The interesting question the essay skips isn’t “how efficient is this?” — it’s “who watches the planner, and what stops it?” The productivity feature and the telescreen have the same blueprint.

The mic-drop: the medium is the message, and the message is the warning

One detail seals it. The gorgeous companion video for this AI-maximalist thesis was, by Patel’s own narration, generated entirely by Google’s Veo model and sponsored by Google — “not a single frame of video was shot.” A film with no humans, arguing that firms need no humans, is itself a live demonstration of the exact synthetic-content loop the Nature model-collapse paper warns about. Reporting on Veo documented the same “lame dad joke” served to multiple users and training data bleeding into outputs — the homogenisation the thesis conveniently assumes away, visible in the pixels selling it. It is, quite literally, an ad. The AGI-firm vision is also a product being sold. The medium is the message, and the message is the warning.

What this means for your trading desk

- Don’t buy “headcount-in-GPUs” as a moat. The durable edge is proprietary data the market generates plus human judgment at the decision point — not a bigger monolith. Audit any AI vendor’s pitch for the hidden assumption that judgment is copyable.

- Engineer for diversity, not monoculture. Correlated models fail together. Run heterogeneous strategies and heterogeneous agents; treat cognitive diversity as risk management, not overhead.

- Keep a real-data pipeline the AI doesn’t control. Model collapse is a systems risk. If your intelligence learns only from its own outputs, its tails vanish and its confidence rises as its accuracy falls.

- Distinguish risk from uncertainty before you throw compute at a decision. Monte Carlo answers risk (known distribution). Strategy lives in Knightian uncertainty. A million simulations of the wrong model is a confident wrong answer, faster.

- Bet on the swarm. Cheap coordination favours networks of specialised agents transacting through prices. Build to plug into that market, not to become the last firm standing.

FAQ

What is Dwarkesh Patel’s “AI Firm” thesis in one sentence?

That once AGI exists, firms become armies of copyable, mergeable, evolvable digital minds directed by a super-CEO, because AI labour — unlike human labour — can be cloned, distilled, and scaled by turning capital into compute.

What is the strongest objection to the AI firm idea?

The knowledge problem (Hayek, 1945): the information needed to coordinate an economy is dispersed, tacit, and generated by the market itself, so it cannot be centralised into one mind at any compute budget. The AI firm is central planning, and central planning fails for reasons of kind, not degree.

Can AI actually copy human judgment and tacit knowledge?

Not the un-codifiable part. Polanyi’s Paradox — “we know more than we can tell” — means the most valuable judgment resists articulation into training data. You can copy a model’s weights perfectly, but you cannot first get tacit knowledge into the weights; that acquisition is the hard problem the thesis assumes away.

Does the “AI firm” mean one company will take over the economy?

The essay’s own cited theorem argues the opposite. Coase says firms stop growing when internal coordination costs meet market costs; cheap AI coordination lowers both, favouring a decentralised swarm of specialised agents over a monopoly. The 13–15% conglomerate discount is the empirical footprint of over-centralisation.

What is model collapse and why does it matter here?

Model collapse (Shumailov et al., Nature 2024) is the irreversible degradation that happens when models train on their own generated output — tails vanish, variance shrinks, quality decays. It’s the direct failure mode of a firm whose central AI learns mainly from copies of itself instead of fresh contact with real markets.

About RocketEdge

RocketEdge builds AI-powered trading infrastructure for institutional and professional traders in APAC and globally. Our products — MultiEdge AI Signal Fabric, the Agentic Research Platform, and the AI Trade Idea Generator — are built Azure-native and designed around a simple conviction: the edge is human judgment plus proprietary data, applied through diverse, validated systems — not a single monolith counting on copyable wisdom.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Past performance is not indicative of future results. All figures attributed to third-party sources reflect those sources; illustrative examples are labelled as such. Views on the referenced essay and video are offered as good-faith critical commentary.